March 22, 2015

This article is for people who have defaulted on their Sallie Mae/Navient student loans. If you haven’t defaulted, or if you’re paying traditional subsidized or unsubsidized federal loans, this won’t work for you. For those of you that ARE in this position, this post is for you. You can get your life back.

I’m sharing all of my actual numbers, because it makes the conversation more useful.

Managing the chaos

Like many people, I was unemployed in 2009-2010. I had the bad fortune of graduating in the middle of the recession, and had quite a bit of difficulty finding a “big kid” job, i.e. one that would let me pay my bills–including my student loans. Also like many people who are struggling with debt they can’t pay, I was plagued by phone calls, and they were universally unproductive, because stones don’t have much blood to give. The first step to getting your feet under you is to create mental space, and the biggest thing is to stop the unwanted calls.

In addition to sending letters, I did this:

- Get a Google Voice number

- Log into your delinquent accounts, and use the Google Voice number as your only phone number

- Don’t answer numbers you don’t recognize

- Take down each collection agency’s contact information (phone number, debt they’re collecting on, etc.) when they leave you a voicemail

- Block each caller one by one

This builds a strategic rolodex for tackling your debts when you’ve got your feet under you. If getting back on your feet takes a while–it took me 2 years–you’ll notice that debt gets resold fairly often, and as it gets resold, the settlement offers get better and better. This is particularly true for unsecured, consumer debt, and less true with student debt.

Negotiating with Sallie Mae/Navient and FMS

Sallie Mae stops trying to collect debts themselves fairly quickly, and they tend to outsource this to other agencies. Unlike consumer debt, Sallie Mae does not sell the debt to the servicing organization. Instead they retain ownership of the debt, as well as the terms and conditions under which that debt may be settled. (In fact, if you try to call Sallie Mae directly, you will be redirected to the servicing agency without ever having talked to a human being.) The debt collector is just a proxy, but they’re the ones you’ll be dealing with.

My debt was serviced by an organization called FMS. You can Google them; there are many horror stories, but my experience was pretty good, barring a few incidents. I had settled a couple of smaller credit card debts to this point, so I made sure to unblock their phone number only when I had a small lump of money available to make a down payment. I knew I wasn’t going to be able to discuss a full settlement, but maybe I could do something to move the needle in the right direction. This ended up being a good move, though the benefits weren’t obvious until much later.

Default settlements

I’m going to use the term “default settlement” below. I don’t know for sure, but I believe that Sallie Mae’s proxies are authorized to offer some percentage (65-70% or so) as a settlement amount, without phoning the Sallie Mae mothership. The reason I believe this is true, is because they would periodically offer me settlements on the spot which didn’t require them to phone home. This was in contrast to my counteroffers which required a ~24-48 hour turnaround time where they had to talk to someone with more authority.

The reduced-interest plan

June 2011 balance: $144,586.

I brought my account up to date on July 25, 2011 with a $1,493.38 payment, and set up a recurring payment every two weeks for $372.56. This was their “reduced interest plan”, where the interest rate dropped to 0.01%. There was no discussion of a settlement at this point that I can recall. If there had been, it would have been WAY more money than I had, so it didn’t matter.

I made bi-weekly payments from July 2011 to May 2012.

The first settlement offer: the first $80K

In May 2012, I got a phone call from FMS to re-up my recurring payments. (They can only schedule 12 at a time.) At this time, the rep I had been dealing with all along offered me a settlement that was still too large for me to take advantage of in one shot. I told her as much, and if I recall correctly, she conferred with her manager and the Sallie Mae mothership, and they made me a counter-offer: an $80,000 reduction if I:

- Made a $7000 down payment by the end of the month

- Paid $800/month for 45 months

- At the 0.01% interest rate

This dropped the loan term from 155 months to 45 months, a 9+ year reduction. BUT, if I broke the terms, the full balance came back at the original interest rate, minus whatever I’d paid. I went for it, because saving $80,000 and 9 years was too good to leave on the table.

- Settlement starting balance: $45,375

- Made the $7000 down-payment (with my dad’s help) in May 2012, which

- Reduced the amount left to pay to $36,375 (or so I thought, more on that below)

I set up a $400 recurring payment every 2 weeks, including months with 3 weeks to ensure I’d make the deadline with some headroom.

A bump in the road

Unfortunately, FMS wouldn’t send me paperwork stating the terms of the settlement, which (as I suspected) came back to bite me. I also hadn’t recorded our phone conversations, because until this point, there was no reason to think that I would need to.

December 2013 rolled around, and I received a phone call telling me that I was almost out of time, and that I owed like $45,442 by ~February 2014, which didn’t sound right. Unfortunately, I was dealing with a new representative, and she couldn’t decipher the notes of the previous representative. It was my notes against theirs… and when you’re in this position, the other party holds all the cards; you’re just along for the ride, hoping they don’t fuck anything up too badly. (That said, I’m very confident that my notes were more accurate. Not that it mattered then, and I can’t imagine it would have mattered in a courtroom.)

There was about a week of back-and-forth, but the takeaway was that I owed the $45.4K, but that the terms were extended until September 20, 2018. That was a big relief–there was no way my pre-wife and I could have come up with the money in that time.

I made sure to record that conversation should things go awry again. Check the laws in your state… my state is a two-party state which means that I needed the rep’s permission to record the conversation.

The final $20K

Because FMS can’t schedule more than 12 payments at a time, I end up talking to them about once a year. While re-upping my payments for this year, the rep mentioned that for whatever reason, Sallie Mae was accepting settlements “for pennies on the dollar this month”. That’s just a figure of speech, so I didn’t know if that was literally pennies or what, but she asked if I was interested in seeing if they would re-negotiate the settlement, because I’d basically paid $35K already, and was a model citizen. Of course I said yes, and they offered me their default settlement of $24K on the $35K owed on the spot, which is 68 cents on the dollar. I told them I couldn’t do more than $10K–a true statement–fully expecting a counteroffer for somewhere between $10-20K, whereupon we’d have to borrow some money from my wife’s parents. They said they’d have to call SLMA to see if they’d approve it.

The next morning, I got a call back: Sallie Mae had approved the $10K for the remaining $35K. The rep was shocked. The manager was shocked. They told me no one in the office had thought it would go through, which I believe. I get the feeling I’m going to be an office legend for the foreseeable future.

Recap

- $144,586 original balance

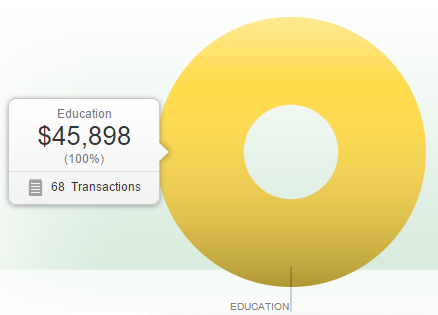

- $45,898 paid over 3.25 years

- $98,688 saved

- 68% discount (or 32 cents on the dollar) when all was said and done

FMS payments

Here’s a Google spreadsheet that shows all the debits over that time. Alternatively, you can download the Excel version.

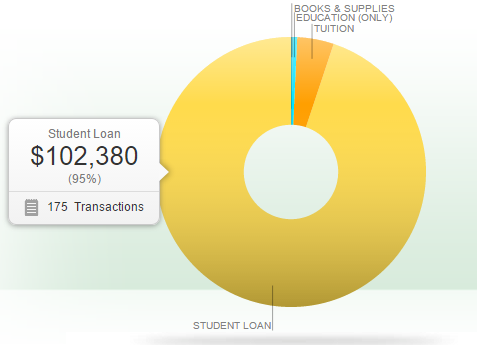

Total student loans paid during this time

I have more traditional subsidized and unsubsidized student loans that actually had interest rates, so I focused on overpaying those during this time.

Conclusions and tax implications

Once you wrap up your settlement, you’ll have taxes to pay. In my case, my income tax burden for 2015 is now my salary + $98,600, which is… a lot. Depending on where you are financially, you may be able to reduce the canceled debt “income” by whatever your net worth is, if it’s negative by filing a Form 982. To determine if this is available to you, you can fill out the worksheet on page 8 of this IRS form. If the sum you come up with is negative, you can subtract that amount from your paper “income”. (I suggest you talk to an accountant if this applies to you, though.)

Other options include maxing our your pre-tax retirement contributions (401k/403b), and/or using your FSA plan to do something expensive like getting the LASIK you always wanted. Unfortunately, doing this latter thing requires knowledge ahead of time that you’ll be settling during this particular FSA year.

Otherwise you’ll want to adjust your tax withholding, because you’ll pay an underpayment penalty in addition to the tax on this “income” if you don’t pay enough tax throughout the year.

So I settled on a settlement saving my wife and I about $100,000 and ten years. This will let us buy a house and start a family years earlier than we had thought we’d be able to. I think my situation may be unusual, but I don’t believe for a moment that I am a beautiful and unique snowflake. Three and a half years ago, my Sallie Mae situation seemed hopeless, and now… it’s over. It took a lot of hard work, and an unwavering focus to get here, but it can be done.

If I can do it, so can others.

Addendum – June 1, 2015

I wrote this article back on March 22 — 3.5 months ago. I had expected to be able to publish this much earlier, when I got the statement that our business was concluded. During this period, a few things happened

- I never received the paperwork stating that I had fulfilled my side of the deal

- Sallie Mae/Navient and FMS parted ways as business partners, which made it harder for me to get information from either one of them

- I had to fight with Sallie Mae/Navient in an attempt to get them to send me paperwork. They never did. When I talked to them on the phone, they stopped allowing me to record our conversations for some reason

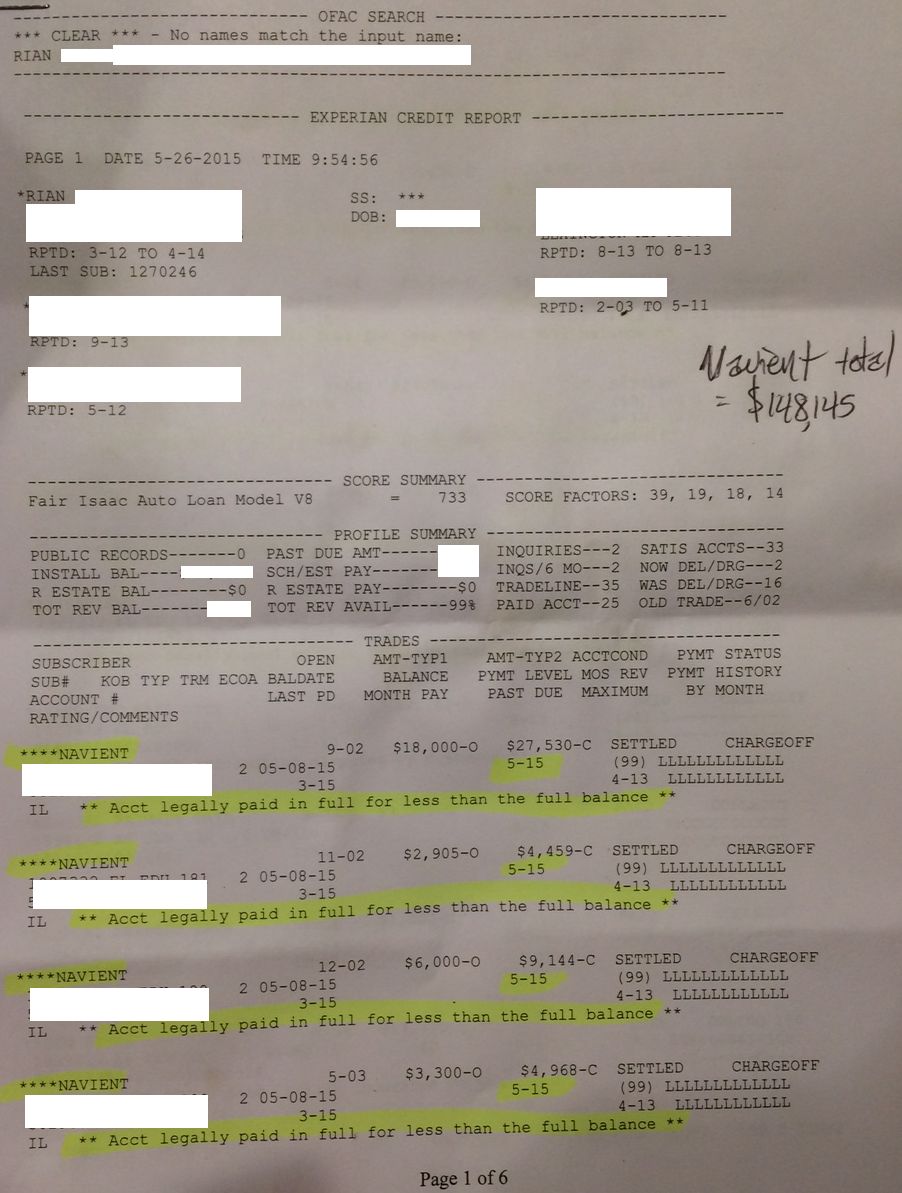

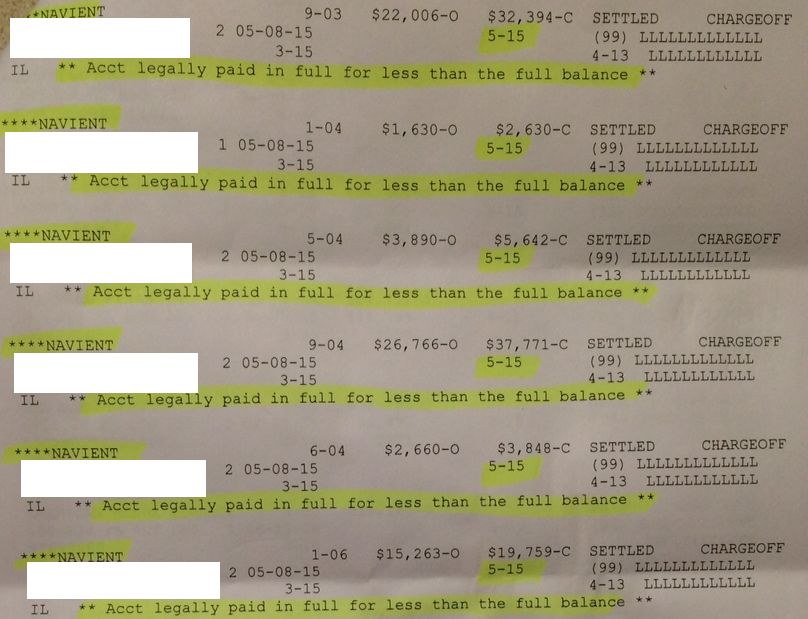

Until today, I had no idea whether this was really done or not. I pull my credit report every year, and was expecting to wait until the summer in order to see if the status of my Sallie Mae/Navient loans were changed. But I bought a new car last week, and part of the financing involved the dealership pulling my credit report, which I was able to take a picture of. It indicated that the loans were settled for less than the balanced owed.

{kind=link}

{kind=link}

I feel reasonably confident that this is the end. Finally.

Leave a comment

- If it’s your first comment on my blog, it will probably go into the moderation queue. Don’t worry, it’s not lost; I just need to approve it. It could be a few minutes, hours, or days. I will get to it, though.

- Try to explain how your situation is different than people that have commented before you. Questions that amount to “I owe money, but can’t afford payments. What should I do?” aren’t constructive.

- I will assume all questions are about private loans only. Federal loans are a completely different kettle of fish.

1099-C update – Feb 2, 2016

I received ten(!) 1099-C forms from Navient on Jan 28. When I reported them on my taxes, I collapsed them down into a single entry for the total amount. I also filled out insolvency Form 982. I was deeply insolvent at the time of the discharge, so instead of paying income tax on an extra $115,282, I only paid income tax on $32,313, because I was underwater by $82,969.

I used TaxAct, which made the process very straightforward. I collapsed the ten forms into a single line item because TaxAct cannot handle more than five 1099-C forms, and their Form 982 worksheet can only be applied against a single line item. We’ll see if the IRS complains. (I don’t know why they would:- the numbers are identical whether they’re reported across ten line items or one.)

Settlement amounts from other readers

- $30K for $8K or 27 cents on the dollar – Jan 2016.

- Update Feb 2017: his tax bill was $6,500–$4,500 federal / $2,000 state

- JKÂ owed $107,000 and I asked them to settle for $8609 which was 10% of the unpaid balance before interest. It was accepted the next day and paid.

I think my loans were private Stafford something or other. I don’t remember what the name of the loan type was.

I would suggest you read my post, and my responses to some of the people here in the comments. If you have a more specific question that isn’t already answered, feel free to ask.

I don’t know, and it’s something I’ve wondered for a little while. Some of my what-ifs are “What if I had ignored the loan(s) entirely? Would they have eventually been written off? Would they have generated a 1099-C?” I think you may be right — they would have expired under the SoL in MA. I suspect there would have been a 1099-C in that situation, too.

I’m not a lawyer, and it didn’t occur to me to look into the difference between private loans and federal loans until much later. I assumed that my wages (once I had them) could/would be garnished, and I didn’t want that, so I engaged Sallie Mae/Navient a little earlier than I would have today based on what I know now. Unfortunately, most online discussion doesn’t differentiate between federal and private loans with respect to repayment/settlement/management strategies. It’s an important distinction, though, as you note.

okay so sallie mae took money out of my account 3 in one month. made my bank go in to default. they said its not them its navient.. then in 2010 i got sick of them collectors and the amount would never go down they would all say it applies to interest not principle.. so i got a loan to pay it off 6,000 then the for the taxes at the end of the year they sent me one for sallie mae and one for nallie mae yes nallie mae they will not amend it because ” we are not nallie mae” well there is no nallie mae its the year they switched to navient. Now all the loans they”consolidated” are coming back seperate again… and I owe the irs. and sallie mae has picked up two of my other accounts using same account number i have been fighting this for ever. im sick of it.. please help

I have over 89k in loans with Sallie Mae/Navient and I thankfully found out about the statute of limitations rules for private student loans! Private loans are considered simple promissory notes, and are not afforded the same protection to the lender as federally funded student loans. Fortunately I cannot be sued, my wages cannot be garnished any longer. Unfortunately the sit on my credit until 7.5 years from date of first delinquency, so another year and a half.

Rian, thank you for sharing your experience. I’ve read everything, and I’m sorry if I’m being repetitive. I have been in default for close to 4 months with Navient, private student loans for $106,000. Interest only payments are $800 soon to be $1,000. Did you ever deal with an attorney, or you did everything on your own over the phone with them? How long were you in default before they would negotiate?

I have federal loans consolidated with myfedloan.org and I also have another balance with AES for $15,000. I’m ok paying only those loans for now (interest only) at about $400 per month. Did you negotiate the federal loans too?

Just to confirm, negotiation only takes place after you’re fully in default. I do have cosigners, but for 5 out of my 10 total loans.

Hey Rian,

I appreciate you taking the time to answer every single comment here. I will cut to the chase now.

I owe $85.000 between 3 different Private Loans with Salie Mae and I have to pay them $935.11/month, which I can’t afford. My family has been helping me but that hast to stop. Now, I’m Peruvian and I recently had to come back to Peru due to the fact that my work permit expired and I wasn’t gonna stay there illegally.

I recently tried to settle through a 3rd party company but I decided to cancel that process on time before signing anything or giving them legal power to speak for me. After reading your post I think there might be a solution to my problem…hopefully.

I have a co-signer who is a US citizen and has good credit. My credit wasn’t good enough to get the loan alone. I just want to stop paying them and wait until they reach back to me in a few months with a settlement plan but the co-signer is in between us and I don’t want them harassing her nor making her pay my debt nor do I want her credit to suffer so much. What can I do? I graduated on October 2013 and was allowed to work in the US for a little over a year until they sent me back to Peru. There is no way my job here can cover even 3/4’s of those $935.11/month.

What happens to my co-signer if I don’t pay? Also, what are my chances of settling right now directly with them and how do I approach them?

I appreciate it a lot, Rian.

Your cosigner’s credit score will take a hit, and your lender will call her almost as much as they would call you. As with all debt, however, she can send them a cease and desist letter, and deal with them only in writing which cuts down on the stress.

I think your chances of settling while you’re in good standing are slim, but there’s nothing stopping you from trying. If you have any luck going from good standing to settlement, I’d love to hear about it. It could help other people who find this page.

This is the best information on negotiating/managing private student loans I’ve ever read, and I’ve been scouring the internet on the subject for years. Thank you!

Two questions:

1) Two of my three private Navient loans are now being serviced by a “collections agency,” and I’m currently ignoring them until I have a good lump sum to offer as settlement. Should I stop paying my third loan until Navient outsources it to a collections agency, then try to settle later on? I can comfortably afford the monthly payment, so it seems like a crazy strategy. But based on everything I’ve read here, it seems like it might actually save me money in the long-run.

2) About what % of the total amount do you suggest offering the collections agency as a settlement amount? It seems like you can settle for as little as 25% in some cases based on the stories above, which is amazing.

Thanks again!

It could save you money at the expense of your credit score. If you can comfortably afford it, I would suggest continuing to pay it, because after you settle, you’ll want some kind of way to build new, good credit history. This is as good a way as any other.

(I also think you should pay loans you can afford to pay, however I recognize that those are my values, and not necessarily yours.)

I would let them make you an offer, and then counter with like half of what they offer, and see what they’re actually willing to take. If it’s in your price range, take the counter. If it’s not, wait and keep on saving: the amount they’ll ask to settle will probably drop over time, even as your savings go up.

Hello. I’m in a similar situation. When they offered you a settlement, what did the paperwork look like? They’ve offered me a 40k payment on a little over 80k. It has their letterhead but the name at the bottom is “Navient collections” and no signature. I’m concerned the signature would come back to make it not count or something.

Per my article, there was no paperwork. It was all done over the phone, which even now I’m not happy about, because I would have liked a paper trail.

I suspect not having a signature is fine. I question the value of signatures in this day and age. Anyway, you’d need someone with the authority to enter into a binding legal contract’s signature anyway, which probably isn’t a thing. Usually those people are VPs, which is why you see so many VPs at financial institutions.

Thank you for good information and for helping us get a shift in perspective. This is the best we can do until either the laws are changed, student debt is forgiven, or we all stop paying en masse.

The student loan predicatment is the end result of neoliberal policies which privatize basic resources and all social goods, transferring the cost onto the individual.

We are living in a time of great inequality; our country has become an oligarchy. Student loans are just another form of debt slavery. The lenders deliberately craft their policies so that the loan continues to grow no matter how much someone pays…they want monthly cash-donors for life.

Well, the tide is turning, and there is a new consciousness arising – millions no longer will stand for the rape and exploitation of humans, animals, or the environment.

The student loan situation is just one facet of human greed for money and power gone awry. Of course, this is exactly what revolution is meant to address. Hopefully, it will be peaceful and waged through the legislative and judicial processes.

But in the meantime, millions of us with student debt are drowning in despair. The most important thing we can do is to remember the situation was deliverately rigged and Sallie Mae spent millions lobbying to have all comsumer protections for student loans removed – especially bankruptcy – so they could do what ever they wanted.

Now that Navient is taking a beating on Wall Street (as they should), wouldn’t it be ironic if they filed for bankruptcy protection?!

If they do, I think we should protest in every way possible to have Navient denied the opportunity to restructure and survive, just as they have worked to deny to all of us.

I just came across your article! What a great piece! I also fell into the same situation as you and luckily I was able to settle 70K worth of Sallie Mae Student loans for a lump some of 8K. I had not made payments since 2007. I just received the 1098-E from Navient.

But my main question is did you ever receive a 1099-MISC from Sallie Mae or Navient to use on your taxes? I want to make sure my taxes are done correctly, but I worry about not receiving this valuable piece of “income” to claim on my taxes.

You would get a 1099-C, not a 1099-MISC. I have not received it yet, either, and I have been googling to see if/when people get them. I haven’t been able to find anything concrete where people have reported getting them, yet. Have a look at the 2015 IRS 1099-C form under the Instructions for Creditor section. It says:

So it should be very soon.

Rian, Thanks for sharing. We really appreciate you telling us your story! I am in a bind myself and seems my situation is getting worse.

I have a few questions:

1) Can Navient harrass my cosigner for payments if my cosigner was released over 2 years ago. Is there a federal law requiring companies to immediately stop attempting to call the cosigner/s if they have been released?

2) How long after did the collection agency contact you after you stopped paying?

-How bad did your credit scores drop? Curious to know how much a person’s score drops once they become delinquent for months?

3) Once you settled, and from the photos you took of your credit report, does the delinquent status stay on your credit report or are they removed once you settle?

4) When you began paying the lower monthly payments that was agreed on, did your improve or was your credit still showing late charges on those months?

Thanks so much for your help and I look forward to your reply!

I don’t know, I’m not a lawyer. That does sound weird, though. If the cosigner was released, they’re no longer on the hook from a legal perspective. But maybe they’re thinking that the cosigner knows you, and can apply pressure to get you to pay. There are many forms of harassment. I have no doubt the cosigner can send them a certified letter telling them to only contact them via mail. That’s probably what I would do.

I’m not entirely sure how long it was between my deferments ended and they started contacting me. By that point, CC companies were calling me several times a day, so I changed my phone number, and didn’t update it with any entity I owed money to so I could create quiet space in my head and life so I could get back on my feet. Sallie Mae probably started at some point after that. So… a year, maybe? Remember, though, this was ~2009, which means lots of people were in the same boat as me, so the bureaucracy was moving slowly due to sheer numbers of defaulted borrowers.

My credit score bottomed out somewhere in the 400s. I think it was like 460 or so. I didn’t pay attention to it during the worst of it because I had more important things to worry about. (Like getting back on my feet.) At no point did I ever sweat my credit score. It is literally impossible to balance settling debt with maintaining a high credit score. It cannot be done. Pick one or the other.

The status goes from “delinquent” to “settled for less than amount owed”. Settled is better than delinquent, but not as good as “paying as agreed” or “paid in full”, obviously.

It was still marked delinquent, because I wasn’t paying Sallie Mae/Navient. I was paying a debt collector working on their behalf, towards a settlement, so there’s no reason the status would have changed. (There’s no “paying towards a settlement” status that I am aware of.) I did, however, continue to get 1098-E forms from Sallie Mae/Navient during this time.

Hi. My student loan has defaulted and now Navient has me in a rehabilitation program (which is on its seventh payment), however I have not yet signed the papers that they keep sending me to officially put me into the program. The reason I am hesitant to sign the papers is because when I do, I will be agreeing to accept their 25 percent collection cost fees (on a student loan that I’ve had for over 20 yrs., totally about $100,000 with interest). The moment I got the letter from Navient saying I was in default, I called and dealt with them, but they said that the original default began about a year ago, and I had 60 days to reply from that original date to avoid getting the 25 percent collection fee. I say that I never received (and certainly didn’t sign for) the original notice and therefore shouldn’t be obligated to pay that fee. They told me to contact Sallie Mae, which I did and they told me to fax a letter to them regarding this (which I’m trying to compose). Do you know if they are obligated to get a signature proving that I knew when the default began? Had I known, I would have dealt with it right away to avoid this huge collection fee. Do I have any recourse?

Hi Rian, this is an incredible resource, and I thank you so much for it. I have about 67k in private loans through Sallie Mae initially taken out between 2002-2007. I have been paying interest only for years, but now that they are owned by navient, I can’t even see what I paid before 2013. Here’s where I am today:

-unemployed with two kids, newly married last year

-my husband works

-I have been paying interest only on my credit card, so I haven’t missed in some time, and we pay off my credit card debt when he gets a bonus, or family Monetary gifts come in.

I was trying to figure out what I owe, all that good stuff today, and if I continue on my path, I’ll have paid over $140k for my original $60k debt and be done paying in 2034.

I want to approach them with a settlement offer. We don’t have any money saved up now, but I might be able to work something out with my father, or put it on my credit card.

I have also reached out to lawyers about status of limitations with this debt, but haven’t heard back yet. I’m wondering what your thoughts are. Of course, my husband and I would very much like to start saving for a house…and not Sallie Mae. Thank you.

Rian, this is the only place on the internet I have found useful information. I am of course on the same boat. International student with 148k on 2 loans with interest rates of 10% and 6% serviced by Discover and originated by Citibank. Minimum payments $1.339, right now on Reduced Payment, paying only interests. My 2 biggest concerns: I work in my home country with a salary on local currency which with the current financial situation around the world has increased the Exchange rate with respect to the US dollar therefore my payments have doubled with respect to my salary. Second concern, I have a co-signer in the US I don’t want to affect.

I have not gone into default, but I think this is an option because like you mention it, I am not having a life of any sort and this situation is sleep depriving me.

What is the process for going into default, should I talk to Discover to let them know about my situation? Should I just stop paying? Let my co-signer know? As an international student would they want a settlement with me or would they turn immediately to my co-signer?

I appreciate all the advice I can get considering I have limited understanding of US law on these matters.

Wow… Here I thought I was the only one with this. I’m struggling to deal and work with nsvient on my private loans with them that are in collection in house. They want a huge lump sum I don’t have but I can almost make the monthly payments.. I wonder if I can negotiate the total settlement amount and the monthly payments with them.

Hi, I just read your blog and it was definitely eye opening! I’ve just reached the point to where reality is sitting in about my student loans. I unfortuantely graduated from college during the recession (2009) as well and incurred 160k of student loans. During that time I let Sallie Mae get to me and became depressed and even filed for bankruptcy as I fought to think of a plan of how to get out of this big huge hole. Well fast forward to today I’ve just completed my bankruptcy and I’m in a little better financial standings but I still cannot afford the $1400 a month demand they are wanting me to pay. I received a call from Navient about a week ago and the lady I talked to offered to put me in a “program” which would bring my payments down to $538 a month. I still cannot afford this. The most I can afford is $350 which I told her and she responded they couldn’t go that low. What would you recommend I do? I haven’t made not 1 single payment since I left school due to my bankruptcy and with the monthly payments being so high. Any suggestions will be appreciated. Thanks for the encouragement.

Hey Rian!!

Im in bad shape at the moment. I owe Navient upwards of $145,000. I have read this entire blog and all corresponding responses.

My only problem is that I anticipate being enrolled in Law School full time by the next upcoming Fall semester.

Do you know if attempting to settle my debts with Navient or actually having a settlement put through affects my eligibility to obtain federal loans or any future student loans for when I start Law School. If so, I would rather continue working with Navient until after I graduate Law School. I dont know what to do…

They are demanding I pay $604 by tomorrow, I dont have the money. I am at a dead end

Hi Rian,

Thank you for a well written article and your thoughtful replies to posters here.

I am in a similar boat and no oars in the water right now.

I have a job which will like my be going away in the next few months. I filed my taxes by an unethical tax preparer and owe $10k to IRS and $25k to state, both take a chunk every month. I live in a high rent state, drive a 15 year old car, etc and there is very little extra income left. I tried paying $75/biweekly which is less per month than the loan payment, but it was something.

I get at least 6 calls a day (cell and landline) and multiple emails from different people at Navient, all of them wanting me to go into forbearance again and that equals more interest and an even higher payment Shen the loan comes out of forbearance. I feel stuck.

You are very right, the system is rigged to set up people to be in debt for life. This ethically and morally very wrong.

I think it would be great if you could talk to Senator Elizabeth Warren about this issue. She has tried to help students with this debt crisis. You are very articulate and are a great resource for those of us needing information on this issue. I think you would be a good public advocate to help change this school loan situation.

I wish you all the best.

Kind regards,

Kathy

I settled my $30K in loans from Navient for $8K. Their initial offer was $16K. I counter-offered $8K. The rep said there was no way they would take less than $12K. They forgot to submit the paperwork, of course, so I had to follow up. But in the end they accepted my counter-offer.

If you’ve been paying them, they won’t engage you at all with respect to settling.

Your cosigner is on the hook for your loans, in theory. In practice it’s often different as they could just as easily refuse to pay. Your situation isn’t a question of law or anything else, it’s a question of what your relationship with your cosigner is. Discover can’t force you to pay — particularly since you’re out of the country — so you could just stop. It’s up to you, really.

Yes, quite often you can negotiate a settlement paid in installments over time. E.g. Pay $45K over 48 months or something like that. If they offer terms that don’t work for you, don’t pay anything. If it were me, I would save up some money that I thought they’d accept, and go from there. The longer you wait, the greater your negotiating leverage.

Don’t make any payments, and change your phone number. When you’re back on your feet, and have a settlement amount you think they might accept, engage them then.

If you settle (for, say, $40K) on a $145K debt, why would they turn around and lend you another $50-150K — that you’re unlikely to be able to pay back a year from now?

Buying yourself more education isn’t going to solve your problem. Unless you’re going to a top tier law school, it isn’t worth it, as the labor market and demand for lawyers is shrinking. Law salaries follow a bimodal distribution clustering around $40K/year and $120K/year. Unless you have some special skills (e.g. health care background + law school) or go to a top tier school, you’re unlikely to do well financially. You’ll probably end up worse off than you are now.

If it were me, I would change my number, and stop paying. You need to get your feet under you before worrying about Navient. Get a job, establish an emergency fund as best you can (even a thousand bucks or so). Have a good six months of stability before even thinking about engaging the student loan company. Better yet, save up a small amount of money that you could plausibly offer them in settlement.

Thanks for the data point! I’m going to start collecting settlement figures, and post them at the end of the blog post.

I haven’t defaulted yet, I have been trying my hardest to pay on these loans, concentrating on my private and putting my federal loans in deferment since I can’t afford both. I have been trying to stay in the rate reduction plan, it took calling my local news station for them to even work with me on that, but since the person I always went with moved, I had to go back to dealing with the generic 1-800 people. I tried reasoning with them, they basically want one of my paychecks every month, even after finding a slightly higher paying job that isn’t retail. I even consulted with an attorney over possibly doing bankruptcy on the private loans, and I hit all points but one. Basically I am at a stand point on what to do, I already am stuck living at home with my parents because I can’t afford an apartment. Do you think defaulting would be the way to go at this point? I’m just worried that Sallie Mae/Navient will end up taking me to court over it and still be in the same boat Im in now.

If it were me, I would stop paying Sallie Mae, and start paying your federal loans. You can default and settle on private loans, but not federal loans. I would let the Sallie loans default, change your phone number, and then build up a settlement that you think they will accept, if you can. I would also work on building a career that will allow me to build something real instead of just barely keeping my head out of the water.

Any energy spent that isn’t focused on building a sustainable career that you can build a real life around is wasted. Everything else is just noise.

Thank you so much for your advice and response. Seriously, you have no idea how much it has helped.

This has given me hope. I had to take out roughly 65k in private loans through sallie mae. We originally agreed at a 2.5% interest rate for all 4 of my loans. However, after I graduated, my rate went up to 9.5% and has already accrued over 20k in interest..as of now my monthly payments are right at 1100 a month and I just cannot afford to pay them off. At first I looked at national debt relief and signed up for their 3-4 year payoff program, but I am soon to drop out of their program because I found out that the credit hit would be a lot worse than what I was told AND they don’t usually settle every loan and the amount of money that is built up from late fees from sallie mae adds up to being more than what I would pay NDR. So now im somewhat back at step one..trying to figure out my best option to help pay off these loans. I’m honestly somewhat scared to try and settle because the last thing I want is for them to just say no and me be screwed.

Why is your credit rating a concern? Credit is only useful insofar as you’ll be borrowing money. If you can’t pay your current loans (regardless of whether those are credit cards, car, mortgage, etc.), you shouldn’t be borrowing more money. Credit rating is the LAST thing you should be worrying about.

How would trying to settle (now or a year from now) result in you being more screwed than you are right now? Yes, the unknown is scary. But to this unbiased observer, you would be no worse off for trying.

I am a Senior citizen. Who lost their home and had to file bankruptcy in 2009. I have a Sallie Mae Loan now NAVIENT. I have a consolidated loan of 8% which I was told several years ago that I could lower this rate. The current loan is $43,000 and I have been able to pay them $300 a month for the last year. I just got in the mail that by August 2016 NAVIENT now wants me to pay them $593 a month. This will kill me because I have already reduced as many expenses that I can even not purchasing some needed MED’s so I can continue to pay on this loan. Because of hard times in the economical down size and no jobs in 2009. I got behind and had to defer this loan , and now I have no more deferments. I really would appreciate any assistance that you can share with me. Since this loan is at such a high interest rate of 8%, and was told because it was a consolidated loan, I am not able to reduce the interest rate on this $43,000. Again paying the $300 a month is really a hardship but the $593 a month there no one I can turn to, and I am not able to pay them this amount per month. Do you have any suggestions. I want to pay this loan and have been paying the $293 but there is no way I am able to pay them $593 a month.

If it were me, I would stop paying. Going without medication for the sake of paying Navient is madness. I wouldn’t pay them $593. I wouldn’t pay $300. I would pay nothing.

I defaulted my private student loans with Navient as of Jan 31, 2016. I have been given up to Feb 29, 2016 to decide if I am going to accept one of their offers. My loan balance is roughly $23,000 and a settlement was offered for $12,800 with 20 -30% down and remainder paid over 12 -24 months. The other option is putting down 1390.00 and paying $110 month for 16 1/2 years under a rehabilitation plan. Boy I wish I could take this but its impossible at my current status. I have called many times before and after default, now im faced with being sued if I dont accept something. I am a single parent of 2 and $500 in savings. I did recently received a tax refund but I am catching up other bills. I dont mind paying something but Navient want 1390.00 down by Feb 29. My car need to be repaired, Im so worried that my wages will be garnished. Please help. I need guidance.

Hi Rian,

Your blog is a God-send. I graduated in 2005 with about a total of $50,000 in debt which has now turned into $87,000. From 2005-2011, my loans were in forbearance. Since then, I have been paying monthly and on-time. Unfortunately, they haven’t moved much. Now that I can afford to pay a little extra I have been.

I recently received a call from someone representing Beling Law Firm. They have a private student loan program where you pay them $350 per month and they fight for a discharge or settlement on your behalf. They put your loans in dispute and claim that while in dispute status, it is against federal law to report any negative information including default. Any contact between Navient and and the client (me) is discouraged and they ask that you keep a log because it supposedly strengthens your case. If they can’t get you a discharge or a settlement of at least 65 percent, they use the money that you’ve paid them and apply it to your loans.

What are your thoughts about this? Have you heard anything about it? I can’t seem to find anything on the web about it. Based on what I’ve read, they will probably make my loans default for a little while in order to get me the best settlement. I know you’re not a lawyer but all of you advice so far has been really helpful, so please let me know your thoughts.

Thanks a lot

I think someone else mentioned that firm in these comments. I think they’re basically taking your money, putting it into escrow (which makes money for them) while they attempt to work out a settlement. Then they front the money on that settlement amount, and you pay them on that new, lower balance. (Presumably at some rate of interest.)

You could essentially do the same thing yourself, except if you don’t have the money to front the settlement, you can’t fully close the deal. (I suppose you could engage a p2p lending institution like prosper.com, but I don’t know how much you can borrow from places like that. Or borrow from a relative or something.)

This is just a guess at how it works and what their business model is, but I’d be shocked if I was far off. If this is something that interests you, maybe google around, and see if other people have had success. (Actually it looks like you already did, and couldn’t find much.)

Also beware that a settlement–even via a middleman–will generate a 1099-C on the discharged debt (including the interest), so you will have to pay taxes on that. So assuming they reduce the amount you owe by 65%, you will pay them $30,450, and you will have to pay taxes on an extra $56,550 in income, minus whatever you are insolvent by. Don’t let this scare you away. Definitely look at page 8 of this IRS form. (I really need to turn this into a spreadsheet so people can use it more easily.) I highly recommend filling it out as accurately as you can. If you are in the red (which includes your $87,000 in student debt!), you subtract whatever you’re in the red by from that $56,550. If you have no assets, you’re probably mostly insolvent, which means your additional tax burden will be fairly small. Perhaps even zero.

Anyway. Good luck.

I suspect if you wait, you’ll be able to negotiate better terms.

I don’t think they’re going to sue you right away, if at all. They’re more likely to sell your debt to someone else to collect. Suing is a scare tactic, and is expensive for both parties. I don’t want to say for sure it’s scare tactics, but… it sounds like scare tactics. As I said to someone else a while ago, once your loans get transferred to a different department (or collections agency), the incentives change for the person working your case. (Yes, those agents have metrics they’re trying to meet.)

I’ve not heard of wages being garnished by a private loan company. You might want to google around to see if you can find first-hand accounts of people’s wages being garnished by Navient/Sallie Mae. Not advice columns from people answering general questions trying to drum up business for their legal services, but actual first-hand accounts by real people.

Thank you so much for responding. I hsve been looking everywere online for alternate resources. As I go through this process I will keep you all updated, so maybe it could help someone else.

Thank you Ryan.

Rian: I have 2 consolidated FFEL loans for a total of $70,000 (the original loans totaled $42,000) that went into default in 2012. I have just received a notice from the Guaranty Agency with the balances (including collections) which are now nearly $90,000. I would like to know if they will likely begin garnishing my wages with my employer or when does that happen?

I would like to avoid the embarrassment of wage garnishment and would be completely comfortable with a settlement for the original amount of the loans (or less) paid over the next 4 years with the 0.01 interest you mentioned. I do not have the lump sum so it would have to be a payment plan. Do they work with you on these terms?

Thoughts on achieving this?

FFEL CONSOLIDATED $25,585 01/11/2002 $40,537 $9,654

FFEL CONSOLIDATED $16,049 01/11/2002 $29,694 $7,072

Hi Rian,

I’m helping my 80 year old mother who co-signed on a Sallie May loan for my niece. They/ Sallie made her an offer of $13, 500 on a $15,000 loan. We countered 32 cents on the dollar. We realize that if my mom doesn’t pay it back that it will hurt her credit, but at 80, she really doesn’t need fantastic credit report. Also, can they attach her bank account? I don’t think that my niece will be able to pay this back for quite sometime. Any thoughts you have would be appreciated

You can’t negotiate when it comes to federal loans. They will not play ball, and they WILL garnish your wages, and they do not need a court order to do so. That said, you can rehabilitate your loans, and bring them back into good standing. A simple phone call was all it took for me to rehab my federal loans.

32 cents on the dollar is a reasonable offer. I would be curious to know if they accept, or if they counter-offer. Please reply when you hear back!

And yes, if I recall correctly, you can specify a bank account number and routing number for any account. It doesn’t have to be the one you have historically paid with. What they’ll typically do is set up a three-way phone call with the bank, and verify the funds are there, and that the owner of the account has given their permission for the debit.

My current balance sits at over $100,000 because of capitalized interest. My original principal balance was $32,215. I have paid over $19,000 in 9 years. All of my deferments are exhausted now, and I cannot pay the $1,500/month they want. What is my next step? Thanks for any help.

Thanks so much for your reply! I’m not sure if you have any idea how helpful you are. People our here really need help and there are not many honest options.