So we’re in the open enrollment period for Medicare Part D. It started on November 15, and it ends on December 31. I’ve been doing consulting twice a week, and the scramble is in full effect. While I do quite a bit more than plunk in drugs and quantities for my consulting, there is one tool that is the backbone of what I do when running various scenarios. It’s the Medicare.gov plan finder.

This guide does not apply if you have a hybrid medicaid-medicare plan through your state. Those folks know who they are, and if you have no idea what I’m talking about, you don’t need to worry about it.

Before you begin you’ll need three things:

- A complete drug list of the person you’re doing the research for. This means you’ll need drug names, strengths, and quantities. Calculations are done for a 30-day supply, so if you take something 3 times a day, the quantity for 30 days will be 90.

- About five minutes

- An Internet connection (har har)

Here’s a walk-through, so you’ll want to open the link in a new window or tab…

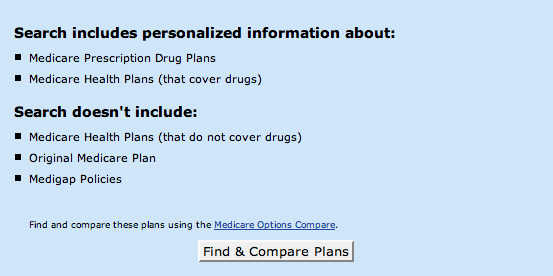

Click on “Find & Compare Plans” which brings you to this:

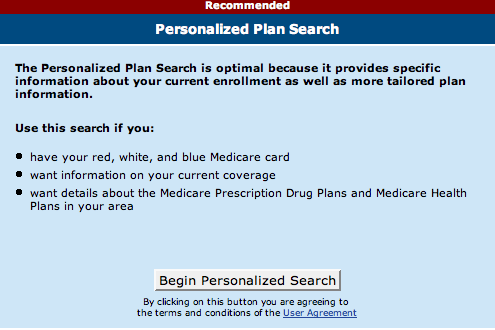

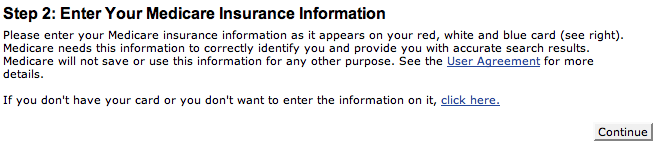

Click “Begin Personalized Search” which will bring you to this next screen. You will want to click where it says “click here.” Do NOT click the Continue button. This might trigger a browser prompt asking you if you want to continue sending this information over an unsecured connection. You’re not actually sending any information about yourself, so click Continue.

That brings you to this page:

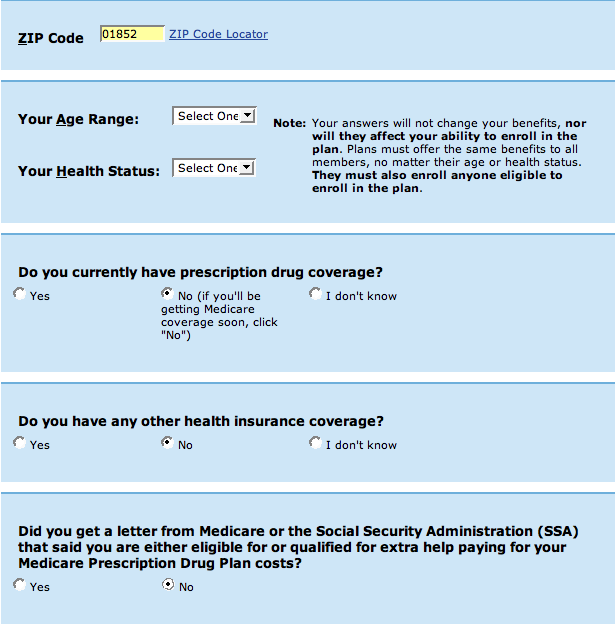

You’ll want to mimic what I’ve done: put in the zip code of the person who you’re doing the search for, ignore the age range and health status, and then select “No” for all three of the next questions. They have no bearing on choosing the Part D plan for the average person. Click “Continue” at the bottom.

That brings you to this. Click the “Continue” button. (Top or bottom doesn’t matter.)

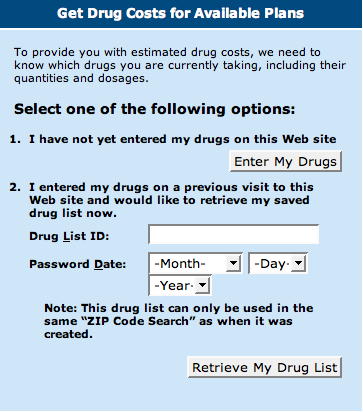

Get out that drug list that you put together. Click “Enter My Drugs” on this screen:

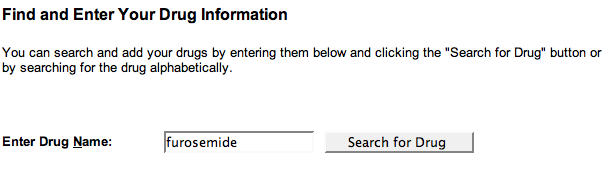

That brings you to this screen, where you can begin typing what drugs you take. I’ll fill in a couple of examples that someone might take, and run you through a couple of screens that you might run into.

So here’s my list for Bob Smith. Click “Continue” at the bottom when you are done filling in the drug names:

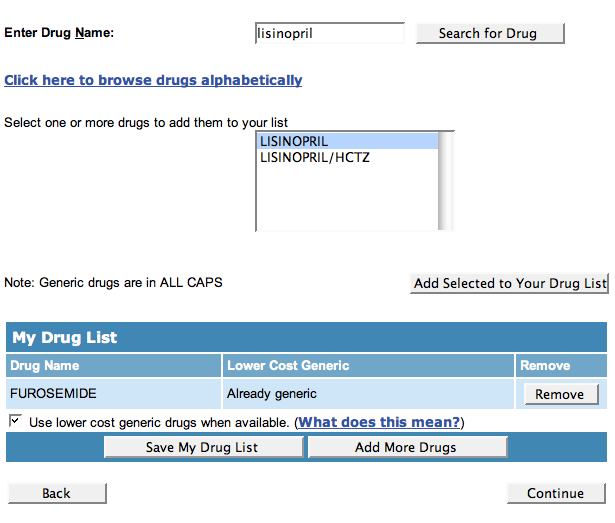

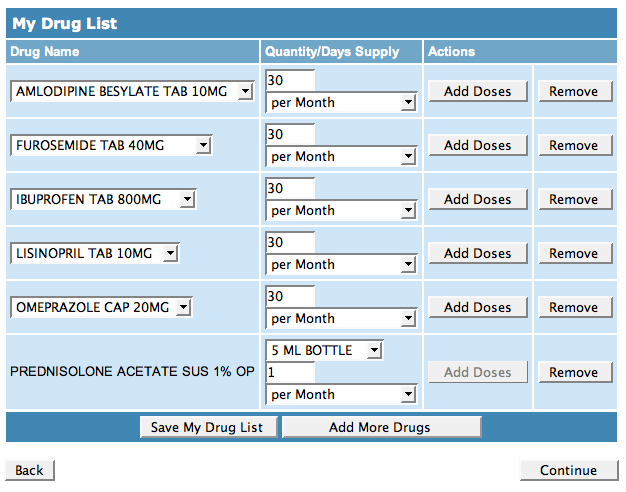

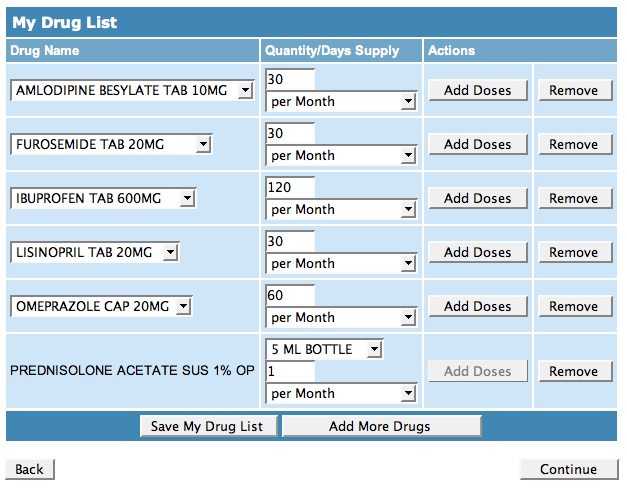

The next screen allows you to adjust the strength and monthly quantity. Go through the list of drugs on the left and change the strengths to reflect the drugs that you use before you start changing the quantities. Each time you select a strength other than the default, the page reloads, and you may lose any changes that you’ve made to the quantity. I learned this the hard way.

This next screenshot is the default, and the one after that reflects the changes I’ve made. Click Continue when you’re finished.

The next step is optional. You can choose a Password Date that allows you to save your drug and location information and pharmacy preferences. That means that when 2009 rolls around, you can more quickly retrieve your drug list and make changes rather than having to enter all of the information from scratch. I recommend using the person’s date of birth because it doesn’t change. I will skip this step because I’m working with a dummy profile, but it is pretty self explanatory.

If you choose to save your drug information, be sure to write down the number that medicare.gov gives you, as well as the date that you chose.

Next you can choose a pharmacy based on zip code. This doesn’t matter overmuch if you’re going to use a chain or independent pharmacy. If you’re working with a specialty pharmacy (for example, your doctor’s office has its own dispensary, or you’re a college student and use the university health office), then you may want to specify the pharmacy that you’ll be going to. Again, I’m going to skip this step since it doesn’t matter for most people.

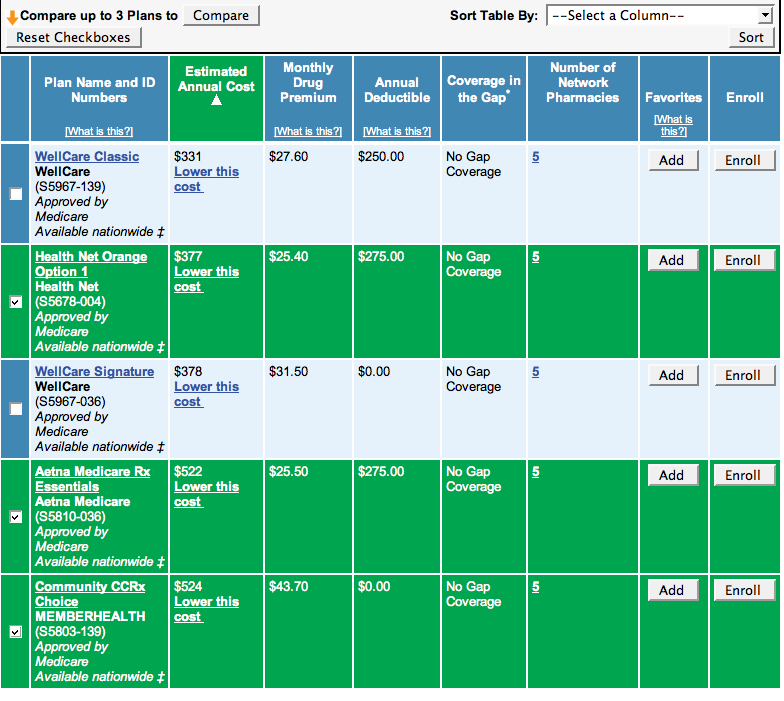

At this point, all of the plans that cover the drugs you entered will show up. I like to display 10 on a page, but that would be a huge screenshot, so I’ll stick with 5 for demo purposes.

You can compare up to 3 plans to see an in-depth breakdown of the plan information (monthly premium, what the copays will be on various drugs and so on. Tick the checkbox for the plans you’re interested in and hit “Compare”. (On every page thus far, there has been a “Printer Friendly” link in the upper left corner. This is particularly helpful if you want to print out the plan summaries and detailed breakdowns for offline viewing and annotating. I use it regularly.)

Plans I don’t recommend

There’s one company that I would avoid right now and that is WellCare. They are the cheapest (as you can see from my screenshots), but they have been in some substantial hot water lately, thanks to some VERY shady accounting practices. Their stock recently plummetted from $130 to $27 at its lowest thanks to being raided by the FBI. They also regularly screw over their customers. Please, stay away from the them.

Enrolling

Enrolling in a plan can be done online or on the phone. Some companies, like Humana, like to send a rep to your house to sign you up. Some people love this, and some people hate it. I find it a little weird, personally. I’d rather call a phone number and do the whole process from beginning to end without having someone come into my home.

[tags]Medicare Part D, How-To, prescription drugs[/tags]

Glad to see someone showing some helpful hints to get the most out of your medicare. I’ve been so angry lately because of the increasing premiums and the fact that a lot of people living on fixed incomes and the elderly cant even begin to afford them! AARP has set up http://www.thisissoridiculous.com

so that we can sign a petition to make our voice heard. You can also read updated news, watch videos, and e-mail your congressman to let him know how you feel!!! Im working to support AARP for better Medicare, this is a serious issue and we cant let it go unadressed!